❋

Diamond Portfolio Review

Due to NDA and confidential information, Figma files for digital access are restricted. Please email me at gs488@cornell.edu for more information.

background

In the past couple of years, Capital One strived to be the best auto lender in the subprime category. They achieved #1 in 2024 and hope to maintain their standing in the subprime lending business and ‘provide the best car buying experience’.

The Diamond Program is a benefits program for dealerships who wish to partner with Capital One on a contractual basis. Being part of the program opens opportunities for more flexibility when negotiating deals and also provides opportunity for dealers (General Managers and above) to earn more participation (a percentage of the deal is awarded to the dealer like a commission).

The partnership with dealers proved to increase revenue for Capital One and increased leads for many of our dealerships. However, we found that overall performance with our program was plateauing, as Capital One started being increasingly lenient with stipulations that would remove dealers from the program to save our existing relationships. Removing the high bar led to dealers taking advantage of benefits provided to them and sending more contracts to other lenders - essentially treating us as their ‘back-pocket’ tool.

In order to save the business and prevent actual losses, I collaborated with the product, tech, and data teams to create strict guidelines and designed a Portfolio Review.

research

In order to better understand the reasons behind the plateaued performance, I wanted to talk to our dealers’ main POC - the Area Sales Managers (ASM). The ASMs are internal Capital One associates, located throughout the nation, who sell Capital One products and maintain relationships with dealerships partnered with us. They do weekly, monthly, or quarterly in-person visits to understand the needs of the dealers and provide dealerships with tools that could drive business.

In my perspective, it was only logical that being lenient would encourage dealers to send us more loans because dealers would see that we value the partnership. I wanted to confirm this assumption and get more insight about what was going on.

I conducted 7 interviews with ASMs and did 12 dealership visits (with an ASM) to get a better picture. Some of the insights I gathered were:

ASMs:

We don’t have the proper tools to talk to dealers about their performance.

We have so many different reports you guys generated for us - we don’t know what to use

I’m too nervous to give dealers the wrong information - I know the dealers like the back of my hand, but I’m not risking my relationship with them by giving false data. How do I know it’s false? You guys have in your system that my dealer has 150 cars in their inventory, but I’m at my location now and can clearly see it’s well over 500. So there is a huge discrepancy in data.

We don’t trust your data and whenever something is wrong with the dealerships and I inform you, you keep telling me to save them.

Dealers:

Leniency = laziness, so why would I send you deals?

Leniency = you’ll vouch for me the next time since you were lenient the past 3 years.

I love that you guys were lenient, but other lenders are providing more participation and their metrics for success are more transparent.

Not enough engagement on how we’re doing with you guys. We send you contracts and you sell us more product we don’t want to buy.

I’ve been wanting to see [info that Wells Fargo is providing], but you guys keep saying this data is for internal use. Why is it private if it’s something we are doing for you guys?

service design + product design

Post-research, I presented my findings to my product team and we agreed that there needs to be a systematic change to the program.

I collaborated with business analysts and the product team to reformulate the diamond program. We decided to do a revamp of the program and form a larger big rocks initiative to rebrand. Though I cannot go into specifics, the revamp essentially redefined the guidelines for what is considered ‘good standing’ with Capital One.

In addition to this program upgrade, I wanted to address the data discrepancy and customer transparency issue at hand. I did 5 rounds of follow up interviews with ASMs to understand how we can improve data accuracy and what they are looking for when communicating with dealers about Diamond Program performance.

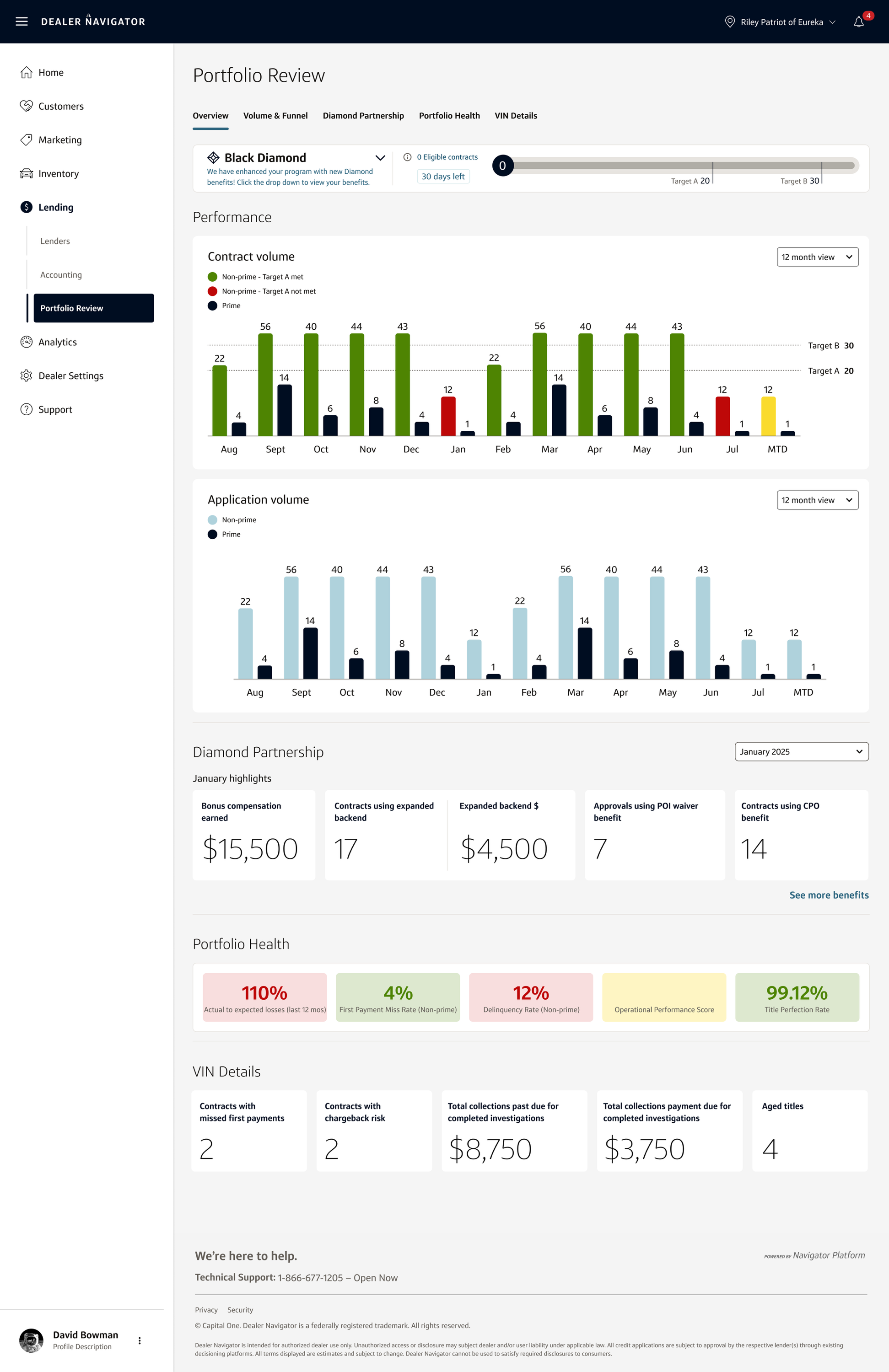

In the end, I designed a Portfolio Review that showcases where the dealers are performing well, how much of our benefits they are taking advantage of, and area where they need to improve in order to maintain good standing with our program.

results

We launched a pilot for the Portfolio Review to be used in 3 regions hand selected by the Dealer Management team.

The first couple of months were challenging due to an internal organizational restructuring. Once the growing pains smoothed over, we saw tremendous progress among our dealers.

After the first 4 weeks:

We saw 38% increase in diamond program policy adherence, 22.3% decrease in delinquencies, and 18% increase in diamond program adoption among new dealers.

Additionally, dealers provided feedback that they love that they can see how they track with our program and also how they are performing compared to their peers. They said, “I want to beat out other dealers so that y’all are more likely to negotiate and waive fees when I’m structuring loans.”

In a couple of weeks, we will be launching the Portfolio Review to more territories and hope to conduct more feedback sessions to maintain and improve this experience for all of our customers.